New Research on Reporting in New Zealand published by the McGuinness Institute

Neil Stevenson (IIRC Managing Director, Global Implementation) pictured with McGuiness Institute publication Survey Insights: An analysis of the 2017 Extended External Reporting Surveys.

Wendy McGuinness, Chief Executive of the New Zealand-based think tank McGuinness Institute, recently visited the IIRC offices in London. She brought with her a number of publications from the Institute’s Project ReportingNZ, which looks at Extended External Reporting (EER):

The term EER is used to encompass disclosures above and beyond what a company is required to provide under New Zealand legislation (Companies Act 1993 and Financial Reporting Act 2013). EER can include information on a company’s outcomes, governance, business model, risks, prospects, strategies and its economic, environmental, social and cultural impacts.

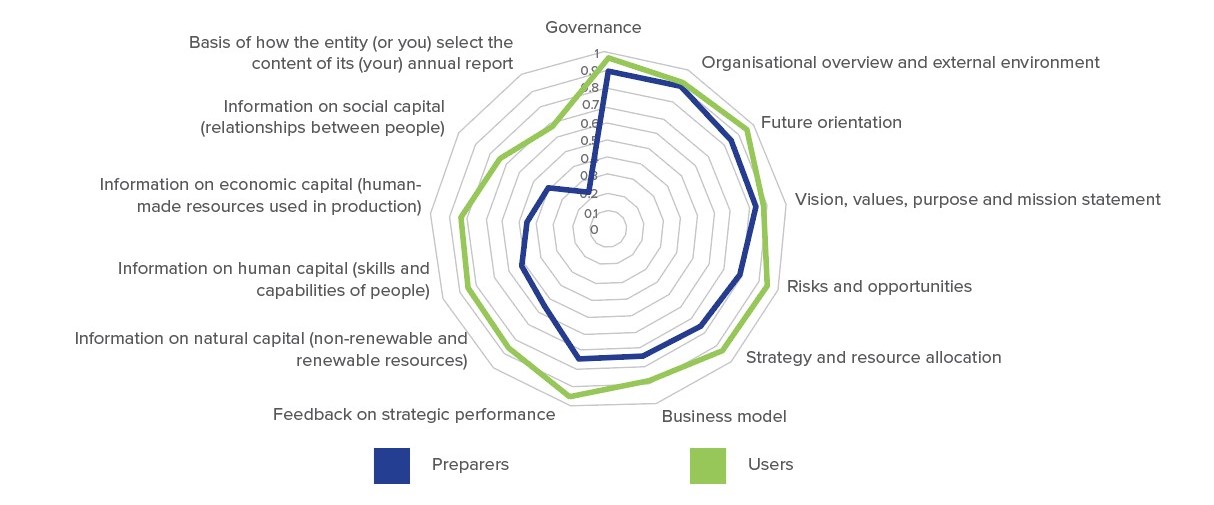

Of particular note is the reliance of the McGuinness Institute’s research on the concepts and guiding principles of the International Integrated Reporting Framework as a way to set the context for the surveys and frame the content of a number of the survey questions. For example, see Figure 1 below from p. 16 of Survey Insights: An analysis of the 2017 Extended External Reporting Surveys.

Figure 1: Preparers’ and Users’ views on content that is considered to be important or very important to disclose

Source: Survey Insights, p. 16

New Zealand could become a global leader in terms of disclosure of this kind of information. This could be achieved by amending legislation to require significant companies to begin reporting on the information outlined in the International Integrated Reporting Framework.

Such reporting is important for creating an informed society that can better respond to risks, yet we found a number of different information gaps that need to be addressed. We expect that, given the current pace of change and level of international complexity, the following information gaps are also likely to exist globally:

- A gap between what Preparers think they are providing (perceived) and what Preparers actually provide (actual). This is indicated by the analysis of the content of annual reports in Working Paper 2018/01 – NZSX-listed Company Tables and the results of the 2017 Preparers’ Survey.

- A gap between what Preparers think they provide (perceived) and what Users think they want (perceived). This is indicated by the difference between the two surveys.

- A gap between what Users think they want (perceived) and what Users actually need (actual). This is indicated by the Institute’s current research matching the Users’ Survey with emerging trends.

Figure 2: The three information gaps existing within the reporting framework

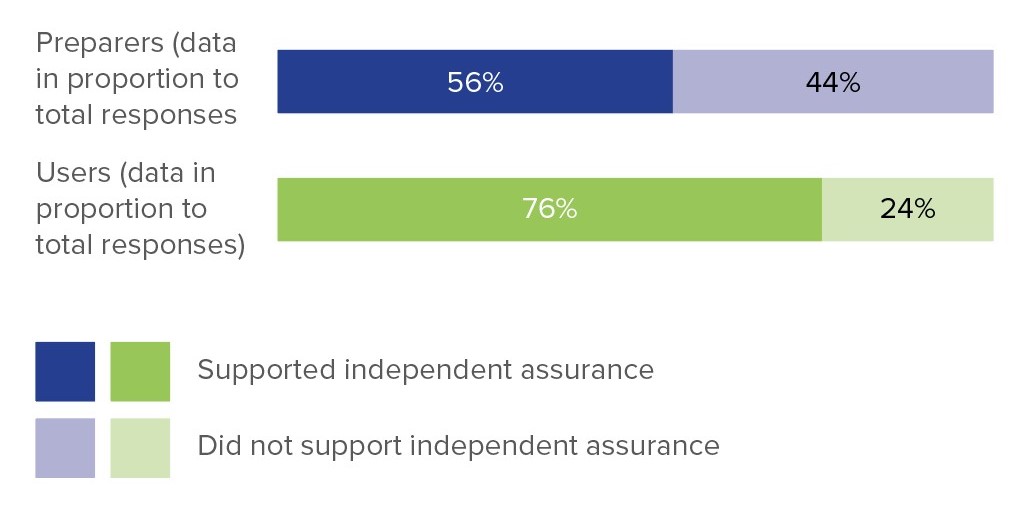

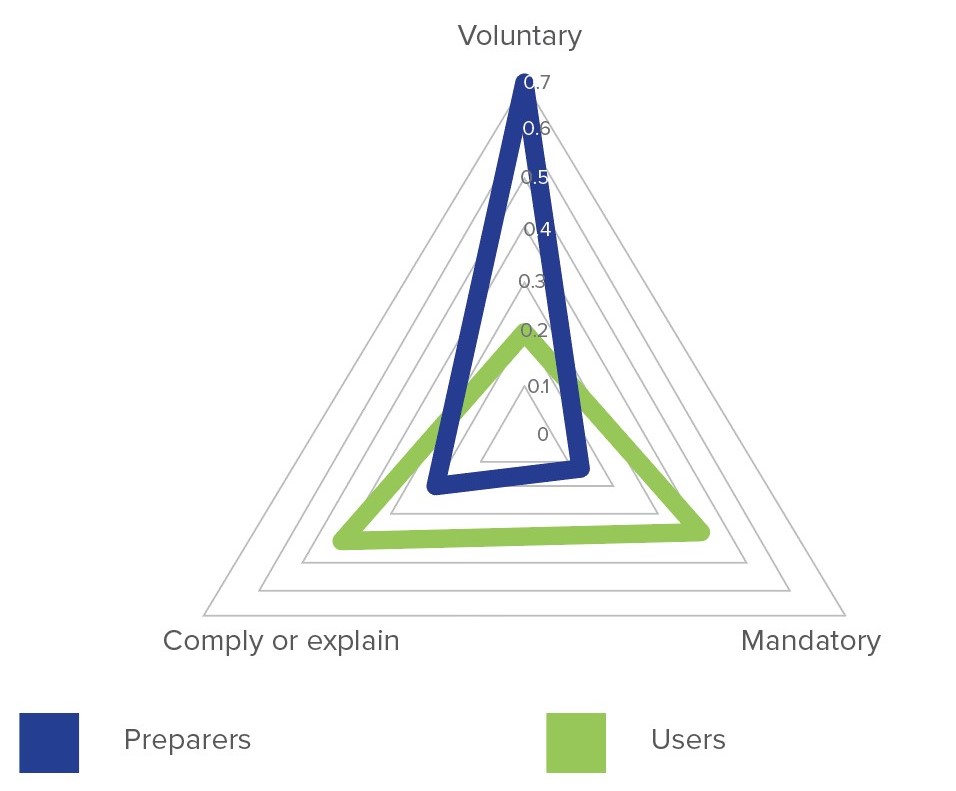

The Surveys also provided interesting insight into the differences between what Preparers and Users think about assurance and whether EER should be mandatory, ‘comply or explain’, or voluntary.

Figure 3: Preparers’ and Users’ views on whether EER should be independently assured

Source: ReportingNZ Overview Worksheet, p. 2

Figure 4: Preparers’ and Users’ views on whether EER should be mandatory, ‘comply or explain’, or voluntary

Source: Survey Insights, p. 20.

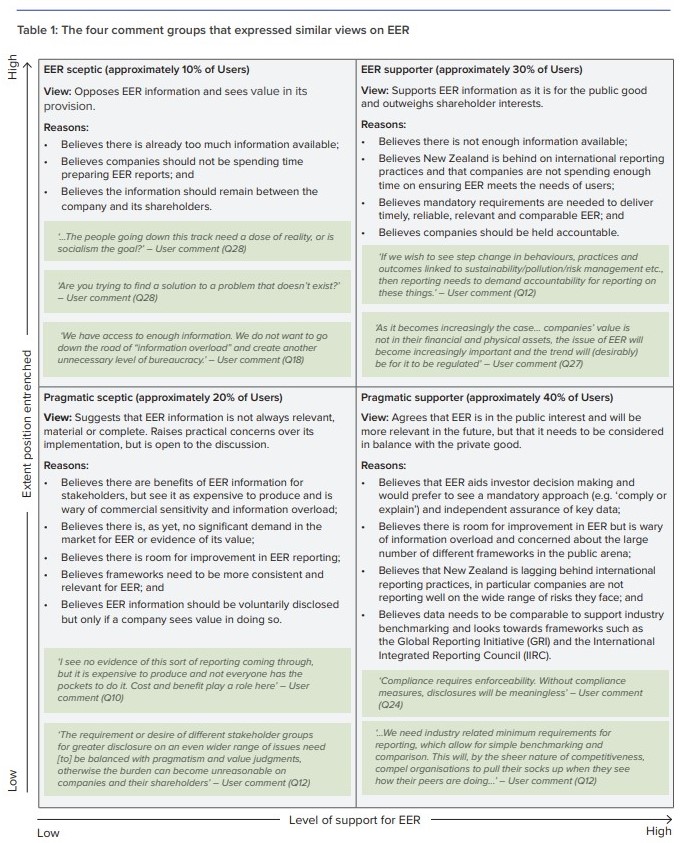

The Users’ Survey comments were of further interest in terms of qualitative insights into Users’ perspectives on EER. Around 70% of Users’ Survey comments were generally supportive of EER (30% of Users’ comments revealing them as ‘EER supporters’ and 40% of Users’ comments revealing them as ‘pragmatic supporters’ – see table below). Comments tended to consider the value of EER in terms of contribution to the public good through holding companies accountable for their actions, as well as in terms of providing better information for investors.

Table 1: The four comment groups that expressed similar views on EER

Source: Survey Insights, p. 9.

About the publications

The McGuinness Institute’s Project ReportingNZ research is made up of seven publications:

- Preparers’ Survey: Attitudes of the CFOs of significant companies towards Extended External Reporting

- Users’ Survey: Attitudes of interested parties towards Extended External Reporting

- Survey Insights: An analysis of the 2017 Extended External Reporting Surveys

- Survey Highlights: A summary of the 2017 Extended External Reporting Surveys

- Working Paper 2018/01 – NZSX-listed Company Tables

- Supporting Paper 2018/01 – Methodology for Working Paper 2018/01

- ReportingNZ Overview Worksheet

The first four publications (pictured above) were prepared in collaboration with New Zealand’s External Reporting Board (XRB):

The Preparers’ Survey and Users’ Survey form the bulk of the data. The Preparers’ Survey was sent to the Chief Financial Officers (CFOs) of NZSX-listed companies (as at June 2017) and the Deloitte Top 200 companies (as at December 2016) and received 92 responses. The Users’ Survey was sent to a wide range of potential EER users including investors, industry organisations, NGOs and universities. It was also promoted on various websites and opened to the general public, receiving 104 responses. The Survey Insights paper analyses qualitative and quantitative data from the two surveys in order to present key insights to interested parties on the current state of EER. The Survey Highlights paper condenses the information further by breaking down the results into what the respondents think about accessibility, engagement, content, frameworks and assurance.

The fifth publication, Working Paper 2018/01 – NZSX-listed Company Tables, was prepared in collaboration with BDO.

This working paper brings together data from 126 2016 annual reports of 2017 NZSX-listed companies to review specific areas of misalignment between current practice and best practice for responsible corporate reporting in New Zealand. The working paper is accompanied by its methodology, set out in Supporting Paper 2018/01 – Methodology for Working Paper 2018/01.

Finally, the ReportingNZ Overview Worksheet brings together key highlights and insights from all the publications in this research project, along with secondary research.

The worksheet presents the seven key research findings:

- New Zealand is not keeping pace with global trends.

- Demand for greater levels of transparency and reporting in New Zealand appears muted.

- Reporting on global risks in New Zealand is weak or missing.

- Climate change and greenhouse gas emissions reporting are missing from annual reports of most significant New Zealand companies.

- Large number of companies are only meeting legal minimum reporting requirements.

- Lack of consistency in format, guidelines and assurance limits usefulness and accessibility for Users.

- New Zealand has a lag in response to international developments in reporting.

It is the Institute’s intention that the methodology developed throughout the research process will allow progress to be benchmarked to analyse how reporting might improve over the coming years.

The Institute has also recently published Working Paper 2018/03 – Analysis of Climate Change Reporting in the Public and Private Sectors, which adapts the methodology of Working Paper 2018/01 – NZSX-listed Company Tables to apply specifically to disclosures of climate change information. The data covers the 2017 annual reports (or financial statements) of private sector organisations listed on the Deloitte Top 200, and public sector organisations such as government departments, Crown agents and Crown entities, state-owned enterprises and local authorities in New Zealand. The results of the research are summarised in a blog post here and the full working paper can be found here.

One of the authors of the ReportingNZ work, Isabella Smith, a research analyst at the McGuinness Institute.