Now is the Time for Companies to Rethink Value Creation. Here's What that Means for CFOs

The COVID-19 pandemic is the greatest threat to value creation in generations. Amidst significant financial loss and looming recessions in 2020 for many countries, many businesses are thinking more deeply about their purpose and value proposition to a wider range of stakeholders. COVID has also accelerated digital transformation, which together with a broader role in long-term value creation, provides a foundation for future-fit CFOs and finance functions.

Company boards and management teams have significant decisions to make in the face of uncertainty, often with imperfect or poor information. The top item on their agenda is balancing the protection, use, and distribution of cash with ensuring long-term value creation and creating a positive impact on all stakeholders. Current priorities for value protection and creation include evaluating the longer-term consequences of the pandemic, such as changes in customer behaviours and demands, shorter supply chains, and digital transformation of operating and business models.

The wider sustainable development agenda, represented by the UN’s sustainable development goals (SDGs), should remain an important focus for governments and business, particularly as systemic risks such as climate change and inequality escalate.

Even before the current crisis, boards, management teams, investors, and other external stakeholders were crying out for better information to help them make decisions for the long term, manage trade-offs, and comprehensively assess corporate performance.

PwC’s 22nd Annual Global CEO Survey reported a large gap between data considered critical or important for decision-making and the comprehensiveness of that data as currently received across a range of areas. This data inadequacy inhibits the ability of board and management teams to steer their organisations on all relevant aspects of value creation. Among the desired areas for improvement are data related to customers, brand and reputation, employees, effectiveness of R&D, supply chain and other key business risks.

Investors and other stakeholders are also demanding corporate reporting that provides relevant, reliable and comparable information on value creation and impact, including non-GAAP measures, key performance indicators, and broader measures related to environmental, social and governance (ESG) performance.

Corporate reporting should capture all relevant information about organisations required by investors and other stakeholders to make decisions on allocating their capital. However, external reporting must be aligned to internal priorities and measurement of value creation and impact.

The Leading Role of the CFO and Finance Function

To contribute to a broader value creation agenda, accountants, particularly those in CFO roles and in finance teams, need to ensure they are not caught in the old paradigm of relying on financial information alone to indicate corporate performance and success. They can use integrated reporting to champion “integrated thinking” within organisations which strengthens management reporting, analysis, and decision making by integrating all of the entity’s value drivers and significant societal impacts.

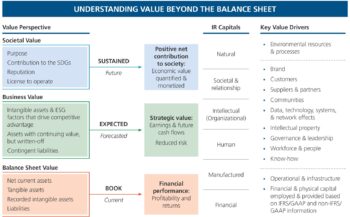

New thinking from IFAC, IIRC, AICPA and CIMA highlights how finance teams can better understand, measure, and report on value creation and impact. It is important for companies to gain a comprehensive picture of value and use this information to drive long-term sustainable success. At least 80 percent of enterprise value is hidden from the balance sheet. As a result, it is poorly understood by both internal and external stakeholders. The key to unlocking this hidden value is measuring, quantifying, and monetizing different value perspectives and then identifying and growing priority areas of value creation.

Many companies adopting integrated reporting have, as part of managing their business in an integrated way, moved to comprehensive and connected dashboards of relevant information and indicators (financial, non-financial or pre-financial) that show value creation and impact across all relevant topics and stakeholders. The KPIs and metrics reflect the critical priorities of the organisation that are incorporated into plans and objectives, as well as into how potential projects are assessed.

For example, Royal Schiphol Group and Solvay, both involved in the International Integrated Reporting Council’s Integrated Thinking and Strategy Group, steer their organisations with integrated dashboards incorporating priority performance indicators.

Data and measurement need to capture relevant “value drivers” and related opportunity and risk factors that affect the prospects for future net cash inflows to the company. Some will be financial value drivers derived from the balance sheet and profit and loss statement, while others will be related to business or enterprise value.

An investor’s perspective of potential for value creation, for example, is driven by:

- Conventional performance and value drivers related to operations and customers

- Relevant intangibles that drive strategic value (e.g., people, IP, data, R&D and innovation, etc.)

- ESG factors that are increasingly used by investors and others as proxies for corporate responsibility and that represent opportunities and risks to value creation.

However, such metrics and KPIs typically track the entity’s gains and losses at the expense of broader organisational impacts and externalities. The link between value creation and impact is an important and evolving area. Societal value is represented by a company’s impacts on the external environment and whether a business has positive and negative impacts on customers, employees, communities, and the environment.

Delivering a Comprehensive View of Value

Many of the impacts that a company has on society are not yet directly material to financial performance or market value, but they do matter to other stakeholders, and increasingly to some investors and asset managers. These impacts also represent opportunities and risks to value creation, but they are not yet fully priced by investors and the market primarily because of a lack of data (and therefore understanding) or the risks playing out over long time horizons. For example, climate risk continues to be largely ignored by investors, according to a recent article in The Economist, but it remains a critical area for many companies to manage and communicate.

In working towards a comprehensive understanding and communication of value creation, management must bring the CFO and finance team in on the journey. They can ensure all functions and business units are aligned in terms of priorities, key indicators and scope, and definitions and controls.

Many companies find themselves sitting on huge amounts of data with no clear view on what drives long-term value creation. The CFO and finance team are well-placed to ensure an integrated view of value, incorporating balance sheet, business, and societal perspectives across all relevant areas or capitals and key stakeholders to enable better decisions and reporting. Prioritising and connecting value perspectives will also help to prevent viewing “non-financial” information in siloes.

The International Integrated Reporting Framework incorporates six areas or capitals which usefully represent the inputs and dependencies for organisations in their value creation process. Companies that are on the integrated reporting journey are generally better placed to incorporate all aspects of value creation, including factors that materially affect future cash flows and therefore market and intrinsic value, as well as to understand the impacts that ultimately support a positive reputation and license to operate.

Rethinking value creation is the key for CFOs and finance functions to become effective partners rather than being perceived as a back-office function. Accounting for value creation will result in a more effective CFO and finance function agenda that shifts the corporate mindset from short-term shareholder value to long-term stakeholder value creation.